India’s steel sector stands at a decisive moment, balancing the pressure of global competition with the momentum of domestic demand and policy support. As producers expand capacity and shift toward green technologies, the sector is positioned to redefine India’s industrial trajectory.

In 2025, India’s steel industry stands at a defining inflection point. Prime Minister Narendra Modi, addressing the India Steel 2025 program in Mumbai, emphasized, “Our steel sector has to be ready for new processes, new grades and new scale.” This vision transcends rhetoric. It signals a profound structural evolution—a shift not merely in output but in essential character. From volume-centric to value-conscious, from bulk production to purpose-driven manufacturing, Indian steel undergoes a reinvention that mirrors the aspirations of a modernizing economy.

This evolution unfolds across multiple dimensions: the advancement of high-end alloy and engineering steel, the expansion of flat and coated products to meet infrastructure requirements, the growth of pipes, tubes and hollow sections for energy and water sectors, and the emergence of stainless steel as an integral component of lifestyle, transport and healthcare solutions. This product diversity serves multiple strategic functions. It shields the industry from cyclical downturns, integrates it with global supply chains, and ensures the steel sector propels rather than constrains India’s broader industrial ambitions.

Scaling Up for a $5 Trillion Economy

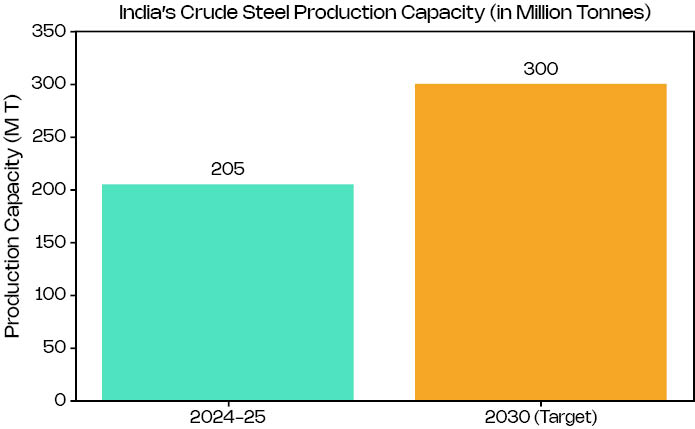

India’s crude steel production capacity has reached 205 million tonnes (MT) in FY25, marking a 10% increase from the previous year. Its crude steel production totaled 151.1 MT in fiscal year 2024–25. March alone saw production of 13.8 MT, reflecting 7% year-over-year growth. The National Steel Policy (NSP) 2017 targets 300 MT by 2030. This ambitious goal rests on large-scale infrastructure projects, urban housing initiatives, smart city missions, and the comprehensive $1.3 trillion National Infrastructure Pipeline.

Kamdhenu Limited, a major player in TMT bars, structural steel, and coated sheet production with over 80 franchise-based manufacturing units across India, exemplifies how decentralized growth is shaping the domestic steel landscape. “India plays a pivotal role in the global steel industry both as a major consumer and producer of steel,” says Sunil Kumar Agarwal, Director, Kamdhenu Limited. “It is the second-largest producer of crude steel, has abundant iron ore reserves, and is a net exporter of steel.”

This growth extends beyond a few prominent companies or regions. It represents a nationwide phenomenon. Greenfield capacities emerge in eastern and central India, leveraging proximity to raw material reserves. Concurrently, brownfield expansions in western and southern India aim to serve export markets through coastal integration. The sector’s geographic diversification brings economic opportunity to underserved regions while generating multiplier effects in cement, power, transport, and capital equipment industries.

Simultaneously, demand is no longer just infrastructure-driven. With the government promoting electric mobility, renewable energy, and electronics manufacturing, steel enters new domains—from battery casings and wind turbine towers to electric vehicle platforms and solar panel frames. Each application requires not just increased steel volume but more specialized, high-performance variants.

Moreover, India’s per capita steel consumption, under 80 kg currently, is far below the global average of 230 kg. This gap represents substantial untapped potential, particularly as rising incomes, housing demand, and rural connectivity drive consumption deeper into tier-2 and tier-3 markets. In this context, capacity expansion constitutes strategic preparation rather than speculation.

From Make in India to Green Steel

The central government’s policy initiatives provide robust support. From Production-Linked Incentive (PLI) schemes to the National Manufacturing Mission and the PM-Gati Shakti Master Plan, India aligns logistics, mining and manufacturing to foster steel-intensive development. The government has also mandated the use of ‘Made in India’ steel in public projects.

Highlighting the sector’s wide-ranging impact, Prime Minister Modi remarked, “Whether it is skyscrapers, shipping, highways, high-speed rail, smart cities, or industrial corridors, steel is the strength behind every success story.”

Government programs function not as top-down directives but as enabling frameworks. The PM-Gati Shakti plan integrates over 16 ministries to facilitate logistics-driven growth. This ensures timely availability of raw materials like iron ore and coking coal while enabling finished products to reach markets efficiently. For an industry as weight- and cost-sensitive as steel, these backend efficiencies deliver competitive advantages.

Simultaneously, the Make in India mandate extends beyond symbolism. It drives demand across all categories—from TMT bars in rural roads to stainless steel in metro railcars, from precision tubes in auto components to DI pipes in drinking water projects. Even small-scale producers of long and structural steel benefit as government projects extend to the district level.

Importantly, these policies advance beyond capacity creation to foster technological innovation. Incentives linked to emission norms, scrap recycling, and value-added manufacturing have encouraged the development of forward-looking ecosystems around steel clusters. Industrial parks dedicated to foundries, forging units, and pipe processing centers indicate a maturing industrial geography, where scale and specialization increasingly coexist.

Import Surge, Raw Material Risks, and Global Trade

Despite momentum, the industry is facing difficulties. India became a net importer of steel in FY25, with imports reaching a nine-year high of 9.5 MT. Most of these came from China and South Korea, putting pressure on domestic producers.

“The country primarily meets its demand for coking coal through imports, exposing the steel industry to global supply chain risks and price fluctuations,” Agarwal noted.

Moreover, Europe’s Carbon Border Adjustment Mechanism (CBAM), set to start taxing high-carbon imports by 2026, poses a challenge for India’s largely coal-dependent steel production.

What makes these challenges acute is their asymmetry. Global producers, especially those with energy subsidies or surplus capacity, can afford to dump products in markets like India. This affects not only primary integrated steelmakers but also smaller players in coated, flat, and pipe segments, who find it hard to compete on price. Meanwhile, dependence on imported coking coal means any geopolitical or logistical disruption, like the Russia-Ukraine war or Red Sea blockades, has a ripple effect across the value chain.

CBAM specifically serves as an urgent signal. It does not merely penalize emissions—it reconfigures global trade based on carbon intensity. Indian producers, many still relying on blast furnace technology, must accelerate their decarbonization strategies or risk losing access to lucrative European markets. The emerging frontier involves green premiums—where global buyers pay premium prices for low-carbon steel, benefiting only those who’ve invested in decarbonization.

Scaling Capacity and Expanding Global Footprint

India’s steel success story rests on its leading producers. Tata Steel maintains a total installed capacity of 35 million tonnes per annum (MTPA) across its global operations, including India, Europe, and Southeast Asia. Within India, the company operates at a capacity of 21.6 MTPA through its major plants in Jamshedpur, Kalinganagar, and Meramandali. As part of its ongoing expansion, Tata Steel is increasing the capacity of its Kalinganagar plant from 3 MTPA to 8 MTPA.

JSW Steel, currently India’s largest steelmaker, commands an installed capacity of 29.5 MTPA and aims to grow this to 38.2 MTPA by FY25 and 51.5 MTPA by 2030. Its flagship Vijayanagar plant alone contributes 12.5 MTPA.

Other major producers include SAIL (Steel Authority of India Ltd), operating five integrated plants with a combined capacity of 21 MTPA; Jindal Steel and Power Ltd (JSPL), which holds a capacity of 9.6 MTPA with a focus on long products; and ArcelorMittal Nippon Steel India, formerly Essar Steel, which runs a 9.6 MTPA plant at Hazira. RINL (Vizag Steel) has a capacity of 7.3 MTPA, while Bhushan Power & Steel Ltd (now part of JSW) plans to expand its current 3.5 MTPA capacity to 5 MTPA. Electrosteel Steels, a Vedanta subsidiary, contributes 2.5 MTPA, and JSW Ispat Special Products, based in Raigarh, adds another 1.5 MTPA to the national output.

These companies also invest in green steel initiatives. JSW Steel plans to utilize energy from a 3,800-tonne hydrogen plant for green steel. Tata Steel continues integrating sustainability measures into its production processes.

Notably, capacity expansion extends beyond primary steel to encompass all segments. Producers invest in hot-dip galvanizing lines, cold rolling mills, ERW and seamless pipe manufacturing, alloy steel melting shops, and forging facilities. This reflects the industry’s recognition that future competitiveness depends on product diversity and downstream integration.

Modernization, Diversification, and Green Energy

To counter these pressures, Indian companies are diversifying portfolios and greening their operations.

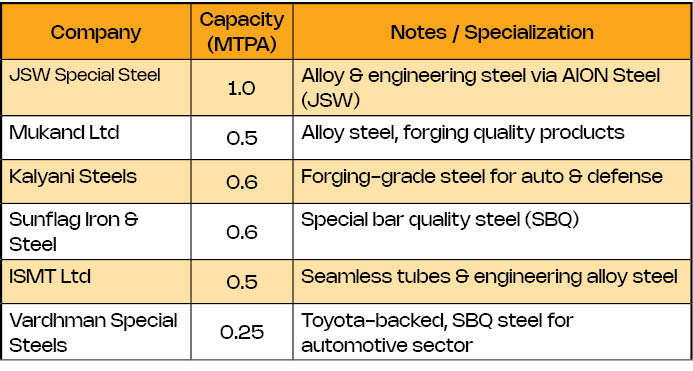

Mukand Limited, a pioneer in India’s alloy and engineering steel segment and the country’s first approved supplier of nuclear-grade stainless steel, is focusing on high-end sectors like aerospace and defense while decarbonizing operations. “We have signed a power delivery agreement for the supply of power from renewable sources like solar, wind and hydro. These sources are likely to fulfill approximately 70 percent of our total power needs,” says Neeraj Kant, CEO.

Similarly, Sambhv Steel Tubes, a rising manufacturer of ERW and GI pipes with backward-integrated capabilities and a recent foray into specialty alloy and stainless steel products, is investing in greenfield expansion and renewable energy. “We have developed the capability to produce steel directly from ore… and set up a 25MW captive power plant to optimize our power cost,” says Vikas Goyal, CEO.

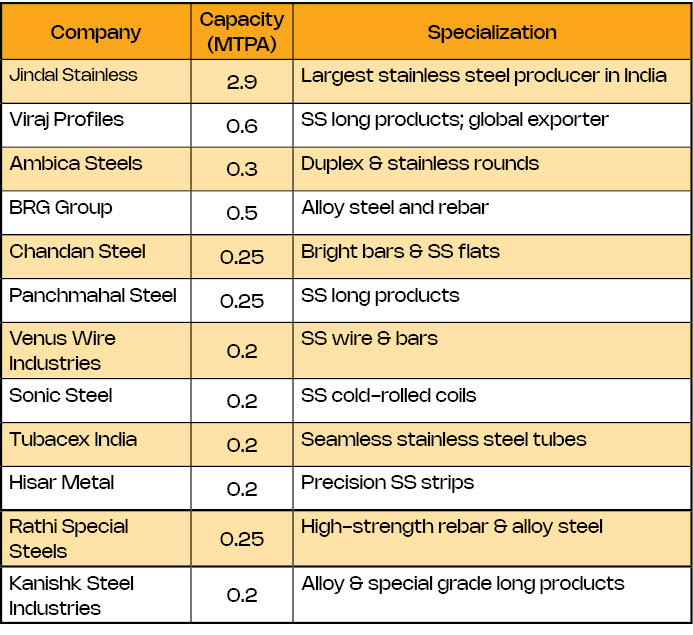

Hisar Metal Industries, a veteran cold-rolling specialist in precision stainless steel coils, pipes, and tubes with an integrated manufacturing setup, is another example. The company is expanding its exports from 25% to 50% and ramping up its solar energy share from 25% to 60% by next year. “The world has shifted its focus towards India and it’s going to remain so for the next 10 years,” says Karan Dev Tayal, Director.

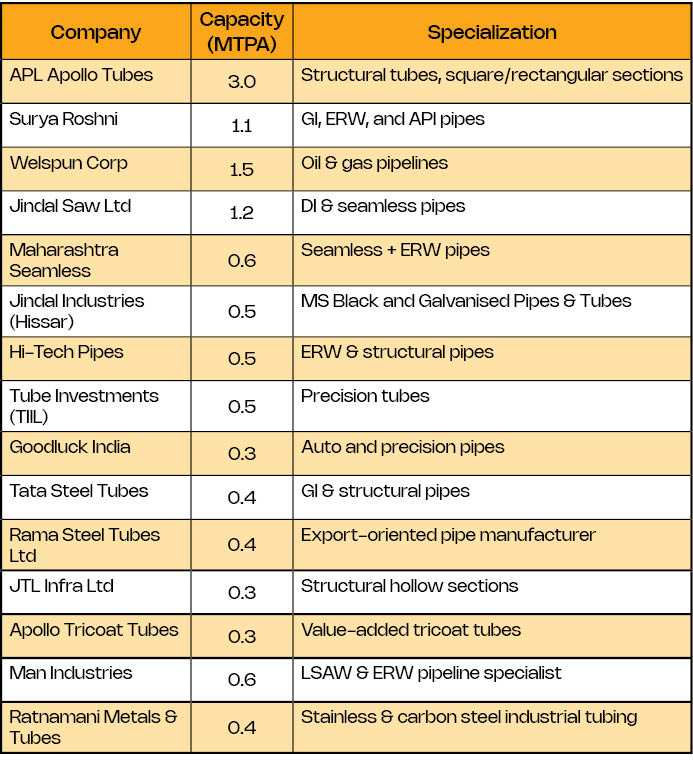

Welspun Corp, a global leader in line pipes, ductile iron pipes, and specialty stainless steel bars and tubes, is investing INR 2,000 crore across India and Saudi Arabia. Its subsidiary, Welspun Specialty Steel Ltd, has achieved indigenous production of supercritical boiler tubes, aligning with the government’s Make in India and green steel vision. “The company also targets 55% renewable electricity utilisation by 2026 and 100% carbon and water neutrality by 2040,” says Vipul Mathur, MD & CEO of Welspun Corp Limited.

Also Read: ESL Steel Gearing Up for Green Steel Production, Focussing on ESG-Centric Manufacturing

Sustainability: The Green Steel Imperative

Sustainability transcends trendy terminology. Indian steelmakers now align with global ESG norms, particularly as the EU’s CBAM approaches. Companies like JSW Steel increase green steel production to comply with emerging regulations. Tata Steel implements sustainability initiatives throughout its production processes. Companies like Welspun target 100% carbon and water neutrality by 2040. Mukand and Sambhv likewise invest in waste heat recovery and solar power.

“Our commitment to sustainability benefits not only the environment but also our customers, employees and stakeholders,” says Neeraj Kant of Mukand.

The green shift responds to consumer demands as well. Multinational customers request carbon footprint data. Investors demand ESG disclosures. Governments offer incentives for decarbonization. Indian companies that act swiftly stand to avoid penalties and secure first-mover advantages.

“Environmental sustainability is integral to our mission for creating a better and greener world,” says Vipul Mathur of Welspun. “… we envisage a significant shift towards new-age innovations by 2030.”

Government initiatives like the green steel taxonomy and star rating on emissions guide the industry toward greener alternatives. With growing emphasis on circular economy principles, companies explore scrap recycling, carbon capture, and hydrogen-based ironmaking as long-term solutions.

A Resilient, Future-Ready Steel Sector

The government has reinforced its commitment to industry transformation through the PM-Gati Shakti National Master Plan and the National Manufacturing Mission. “The government policies and the steel industry are playing a crucial role in the development of many other industries in India and making them globally competitive,” Prime Minister Modi noted.

The road to 300 MT of annual production is not without its potholes. Yet, India’s steel industry has shown resilience, driven by demand, policy support, and private sector dynamism.

“More and more steel companies are coming up in the country, fueling the steel sector growth, which will result in a boom in the manufacturing sector,” says Tayal of Hisar Metal.

India’s steel sector must now focus on technological innovation, environmental stewardship, and global competitiveness. The opportunities are immense—from supplying the burgeoning EV and solar sectors to fulfilling infrastructure needs across Asia and Africa.

In Modi’s words: “India is preparing for global leadership… the world now views India as a trusted supplier of high-quality steel.”

And to rise to that challenge, the steel industry must keep forging ahead—with strength, sustainability, and scale.

Disclaimer: The company listings and capacity figures presented in this article are not exhaustive and intended solely for informational, segmentation, and reference purposes. The data has been compiled from publicly available sources, including investor presentations, company websites, government filings, industry reports, and credible third-party databases. While every effort has been made to ensure the accuracy of the information, the installed capacities mentioned are only indicative and reflect the most recent verifiable figures available at the time of publication. These capacities may have changed due to ongoing expansions, plant-level modifications, or operational updates that may not yet be in the public domain. The placement of companies within specific product or process categories (such as long products, flat products, specialty steel, or tubes and pipes) is based on their dominant manufacturing focus, but does not imply exclusivity in that segment. In cases where direct confirmation from companies was unavailable, estimates have been made in good faith using historical data and industry insights. We welcome and encourage companies to share updates or corrections to ensure that future editions reflect the most accurate and up-to-date information.